What's the secret to Buy To Let investing success?

That’s not an easy question to answer.

But you probably know or have heard of other people that have done it. Right?

You like the idea of creating a portfolio of buy to let properties and earning a significant monthly income.

But how do they do it? Do they know some formula that you don’t?

Well actually, yes they do.

In this guide to investing in buy to let, I will share with you the key golden rules successful buy to let investors have used for decades. Plus: –

- This guide will help you answer the question, “should I invest in buy to let in 2022” and if the buy to let strategy is the right one for you.

- You will discover the implications of the recent changes to tax for buy to let investors including stamp duty for buy to let property.

- Buy to let mortgages are vital to build your portfolio. But how do you work with a buy to let mortgage broker?

- How do you find the best deals and the best buy to let mortgage rates?

- How much deposit is required for buy to let projects?

- How does Buy To Let work and what buy to let rules to follow.

and much, much, more…

So, after reading this investing in buy to let guide you will be able to answer “is buy to let worth it in 2022?” Plus, you will gain valuable buy to let insights that can help you build a successful portfolio of buy to let properties in the UK.

1. What is a Buy to Let?

2. Is Buy to Let worth it in 2022?

3. How to Choose the Best Place to Buy to Let

4. It is Vital to Carry Out Buy to Let Deal Analysis

5. How Does a Buy to Let Mortgage Work

6. Buy to Let using a Limited Company

7. Four Critical Things Buy To Let Investors Need to Know

8. Finding Great Tenants and Managing Your Properties

1. What is a Buy to Let?

The concept of investing in buy to let in the UK is a simple one. You purchase a suitable property that can be let to tenants in return for an agreed monthly rental amount.

Not only does this provide you with a predictable passive income, but you will also benefit from any capital appreciation on the property as well.

When you enter the world of buy to let, you become a landlord, this means you now have a number of legal responsibilities.

You will need to comply with all of the relevant laws and regulations, as the safety of your tenants is of utmost importance. You must ensure any property you rent out is 100% safe.

If you purchase a property solely to rent out to others and not live in it yourself then you can purchase this for cash if you have the funds or put down a deposit and then obtain a buy to let mortgage.

I will go into this in more detail later in this guide.

There may be renovations that you need to carry out when you purchase a buy to let property. However, even if there isn’t, in order to comply with the current regulations, at the very minimum you will need, a gas safe certificate, an electrical installation condition report, an EPC, a fire alarm and a carbon monoxide detector.

Your tenants want to live in great, value for money accommodation.

So, in order for you to obtain the highest rents possible, and get great tenants, that are happy and stay a long time, your property needs to be a high standard.

Buy to let investing is a people business and your tenants are your customers. They need to be treated well and with respect at all times.

2. Is Buy to Let Worth it in 2022?

The number of households in the private rented sector in the UK increased from 2.8 million in 2007 to 4.5 million in 2017, an increase of 1.7 million (63%) households.

So, Buy to let investing is certainly still worth it in 2022, but you need to find the best areas in the UK to make your buy to let investments profitable.

Years ago, you could purchase buy to let properties in your local area and be confident that you would make a good return. Things have changed now.

SOURCE: ONS report on the UK private rented sector: 2018

Buy to let investors feel that they have been unjustly punished by the UK government in recent years and to be honest they have a point.

Changes to Tax on Buy to Let

-

Stamp Duty for Buy to Let Property

You must pay Stamp Duty Land Tax (SDLT) if you buy a property or land over a certain price in England and Northern Ireland.

In Scotland you pay Land and Buildings Transaction Tax

In Wales you pay Land Transaction Tax if the sale was completed on or after 1 April 2018

The government has changed the rules on stamp duty which has resulted in buy to let investors paying increased surcharges.

Since April 2016, buy to let investors have paid an extra 3% in stamp duty when purchasing additional buy-to-let properties.

The surcharge can potentially add thousands of pounds to the stamp duty bill.

| Property Price | Standard Rate | Buy-to-let Rate |

| Up to £125,000 | 0% | 3% |

| £125,001-£250,000 | 2% | 5% |

| £250,001-£925,000 | 5% | 8% |

| £925,001-£1.5m | 10% | 13% |

| £1.5m+ | 12% | 15% |

-

Calculate Stamp Duty on Buy to Let

The UK government have provided an online resource for calculating the stamp duty on buy to let properties, this can be found here;

Calculate Stamp Duty Land Tax (SDLT)

-

Section 24 – Removal of Tax Relief on BTL Mortgage Interest

The UK government have also made changes to the tax relief on mortgage interest. ie they have basically removed it.

Although, lower rate tax payers can still claim a tax credit for the mortgage interest, on the whole this has resulted in increased costs for buy to let investors which they may not be able to totally cover by increasing rents.

The removal of tax relief has been gradually brought in over the last few years, but is now at 100% meaning none of the finance costs can be allowed for in your final years accounts.

This has big implications on whether investing in buy to let is still viable in 2022. It is, but just needs more planning and due diligence, and it is imperative that you speak with a qualified accountant or tax expert.

Where to Buy to Let?

Savvy buy to let investors know that they need to make their investments in areas of the UK that have the best yields and potential for capital appreciation.

The real message here is that you need to be prepared to look further afield for your buy to let deals if your local area does not offer good yields.

Especially if you are in the South East, you may need to “get on your bike” and check out other non-local areas such as in the Midlands, South Wales and Scotland.

If you know your area well and you have good connections in your local area, there then this is going to feel safer for you. But if you really want the best returns then you may need to create these connections in other areas too.

Step out of your comfort zone for the best results.

Despite the coronavirus pandemic there has been no let-up in the demand for private rental accommodation.

In fact, the Covid-19 pandemic has resulted in a shortage of private rental accommodation in the UK.

The well-known London estate agent Hamptons, provided recent data that shows since the start of the coronavirus pandemic in the UK, the number of private rental properties available on the market has dropped by around 300,000.

-

Demand has Increased for Rental Properties

The pandemic has forced people to take stock of their homes and many are looking to downsize to save money or even move out of cities into the surrounding areas.

There has also been an increase in the number of people that are working from home and because of all of the uncertainties that surround the pandemic, a number of people that were considering purchasing a home are now switching to long-term renting instead.

Source: Office for National Statistics – Index of Private Housing Rental Prices

This is all good news for landlords that have private rental property available in the right locations. The high demand for rental properties forces up rental prices and buy to let investors can obtain a higher return on their investment.

Investing in Buy to let is definitely worth it in 2022, if you make the right decisions.

The bottom line is that investing in the UK buy to let market has changed due to the Covid-19 pandemic and other factors.

There will be a shortage of housing in the UK for many years to come and it is very unlikely that the demand for private rental accommodation will decrease any time soon.

3. How to Choose the Best Place To Buy to Let

There is a tendency among UK property investors to invest in areas that are local to them. This does have a lot of advantages, one being that local buy to let properties are easier to look after and manage.

If you intend to become the landlord that does everything to keep the property in good shape then this is certainly true.

But if the yields in your local area are very low, then you are probably missing out on some great cash flow opportunities if you just stay local. Staying local may put a serious dent on your return on investment and could even lead to losses.

Experienced buy to let investors will tell you that the best places to invest in buy to let in the United Kingdom are very unlikely to be just around the corner from where you live.

You may need to take a broader view and be prepared to purchase a property anywhere in the country where the right opportunities exist.

The latest city to top the property hotspot list is Birmingham. Buy to Let in London has fallen way down the pecking order and now trails Birmingham, Liverpool, Leicester, Portsmouth and of course Manchester among many others.

Maximise your return on investment (ROI) by investing in buy to let deals in up-and-coming markets which have the best yields.

As well as a steady increase in prices over the past few years look for new local developments, public transport plans, new schools and so on.

Ultimately, choose a location where your cash is likely to perform at its absolute best.

-

Buy-to-let landlords should focus on income not short term capital growth

Experts assert that rather than investing for short term capital growth buy-to-let landlords should focus on income.

Calculate annual ROI by subtracting your total annual costs from your annual rent. Then calculate yield as a percentage of the purchase price.

- For example, a property that cost £200,000 and generates £10,000 worth of annual rent will have a 5% gross yield. You can achieve higher rental yields than this in other places of the UK right now.

We appreciate that it is not always easy to travel far, especially at the moment with restrictions due to the pandemic. But please do not use this as an excuse.

Make the most of technology and get on the phone to estate agents in the areas that you are interested in. It is not going to be easy, but anything worthwhile rarely is.

According to UK property investment experts, Joseph Mews, the 10 best places to buy to let in the UK that you need to focus on for the best rental yields in 2022 are:

| Location | Average Rental Yield |

| Birmingham | 6.56% |

| Manchester | 6.53% |

| Leeds | 5.76% |

| Leicester | 5.31% |

| Glasgow | 5.31% |

| Newcastle | 5.23% |

| Nottingham | 4.92% |

| Liverpool | 4.82% |

| Sheffield | 4.45% |

| Derby | 4.2% |

Note these are just in order as far as average rental yields are concerned. There are many other factors to take into account when you are choosing the best places for buy to let investments.

Birmingham is in the top spot because average rental prices have increased 30% in the last decade and are predicted to rise by over 12% in the next five years.

In addition to this, Birmingham is seen as the place for people living in London to relocate to, and there are other factors too such as the extension of the Midlands Metro and HS2 train links.

When it comes to the North West of England, Manchester is viewed as the best place because of the quality employment opportunities and the large scale regeneration planned. House prices in Manchester are forecast to increase by over 28% in the coming years, the highest in the UK.

You need to be aware of trends in UK cities and any developments that are planned. A good example of this is Liverpool, where the L1 and L7 postcodes are really popular and have delivered high rental years of 8% and 10% respectively.

4. It is Vital to Carry Out Buy to Let Deal Analysis

As a professional buy to let investor, it is imperative that you know your numbers. Make sure you know the average cost of properties in your chosen area and the rents that you are likely to receive. Aim to cover at least 125% of your mortgage repayments and go higher if you can.

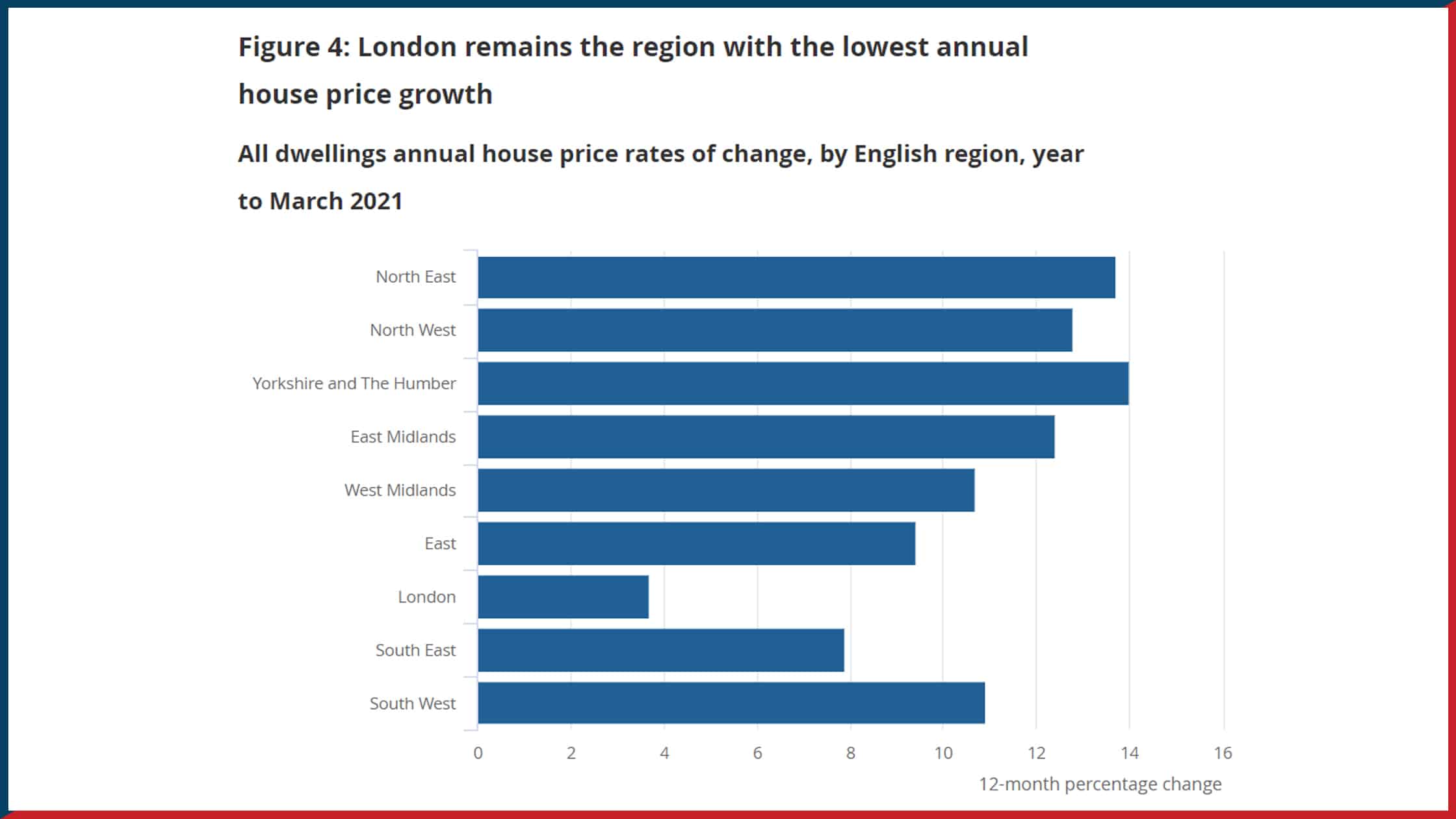

Source: Office for National Statistics – UK House Price Index: March 2021

Source: HM Land Registry – UK House Price Index summary: March 2021

Buy To Let Return On Investment

Return on investment (ROI) is a concept that you really need to grasp, and it is pretty simple to do this.

If you invested £1,000 over a year and you made £100 at the end of the year, your ROI would be 10%.

How to Calculate Your Return on Investment

To calculate the ROI, you simply take the annual pre-tax profit (income minus expenses) and divide it by the total initial cost of the buy to let property (purchase price + closing costs + refurbishment fees).

Buy to Let Return Calculator

Although it is always a good idea to understand the formula behind the metrics we need for profitable property investing. My buy to let return calculator below will help you work out the accurate return on investment for your existing property or a new potential deal.

You can either enter data in all of the boxes or just the Purchase Price, Total Annual Revenue and Total Annual Expenses fields.

Buy to Let Cash on Cash Return

One of my favourite analysis metrics is cash on cash. It provides a measurement of the return based on the total cash invested, rather than the purchase price. This is useful because most of us will utilise mortgages to purchase buy to let deals, and therefore only need to take into account the deposit amount.

The cash on cash return is measured by taking the annual pre-tax cash flow (income minus expenses) and dividing it by the total cash invested (buy to let deposit + closing fees + renovation costs).

So, if you put down a £30,000 deposit on a buy to let property and you were able to realise £500 a month in net operating profit this would mean £6,000 per year.

Your cash on cash return on this deal would be 6000/30000 or a 20% return.

This CoC of 20% does not include any appreciation on your property, or any other factor such as tax breaks and other incentives. It is simply a cash on cash return.

It is better to keep it simple like this, so that you can compare it with investing your money in other ventures.

Analysing Buy to Let Profit and Cashflow

Using the 1% rule. This rule states that you should be able to earn rental income from a property that is at least 1% of the price that you paid for it on an annual basis.

So, if your buy to let property will set you back £200,000, then you must be confident that you can earn at least £2,000 a year in rental income from it.

I recommend the minimum monthly profit on any buy to let property should be £200 a month. You will want to use your own rule here. Maybe 2% is more comfortable for you, or possibly more.

Whatever rule you make, if the buy to let property doesn’t pass this test then just walk away. This is a very quick way to analyse a buy to let property investment.

First and foremost, the numbers need to stack up. Put simply, your cash flow on a buy to let property is what you have left after all of the expenses have been paid. So, if your rental income is £1,000 a month and your outgoings are £800 a month then you have a positive cash flow of £200 a month.

Some people are tempted to factor in the capital appreciation of their properties into this equation. It is obviously a great thing when the value of your property goes up, but you cannot rely on this.

It is best not to use it in any analysis that you do. Just treat it as a very welcome bonus if property prices continue to rise.

A good way to estimate cash flow is to assume that the expenses on a buy to let property, excluding the mortgage payments, will account for 50% of your rental income.

This is best illustrated by an example.

Let’s assume that you are interested in a buy to let deal that you know can bring you in £2,000 a month in rental income.

The reason that you want to factor in 50% non-mortgage costs, is because over the long term you have to take into account maintenance and other costs, and cover for void periods where you will not have rent coming in.

So, if your mortgage payment is £500 a month, you can fairly accurately predict a £500 monthly contribution to your net operating profit (cash flow).

£2000 x 50% = £1000

£1000 – £500 (mortgage costs) = £500

You may be thinking that 50% is a lot for non-mortgage expenses, but experienced buy to let investors tend to use this for their calculations. Some months the expenses will be a lot lower and others will be higher.

Use Deal Analysis Spreadsheets or Software

Once you start to investigate different areas of the country and connect with more estate agents it is likely that you will have a lot of offers to review.

I recommend that you create a simple deal analysis spreadsheet that you can just plug the numbers into so that you can see immediately whether a property is worth investigating further.

You will need to be aware of all of the costs associated with buy to let investment in order to make your spreadsheet as accurate as possible.

Buy to let tax such as stamp duty is important to know about as is the cost of buy to let property insurance. Make sure that you factor in all the likely fees and costs.

Your Buy To Let Goals and Action Plan

Whilst we are talking about numbers, you need to have clear long-term financial goals for your buy to let portfolio.

The government and others have certainly made investing in buy to let more of a challenge now.

A few years ago, it was a lot easier to purchase a rental property and rent it out.

Buy to Let investing has no doubt been hampered by the current market situation and other legislation recently brought in by the Government.

But if you are prepared to stick around for a few years then there is still a lot of money to be made.

Have a clear reason for getting involved in property investment. You need a big “WHY” and you then need to set your goals to be sure of success.

After you have set your buy to let property investment goals then create a plan to achieve them.

There are a number of ways to invest in buy to let, including the standard vanilla strategy (renting to one household), Houses in Multiple Occupation (HMO) or even property funds.

If you are looking for a higher profit potential from your buy to let property, converting it into an HMO could be worth considering.

However, be aware of the responsibilities associated with each path. Looking after HMO tenants and regulations can really sap your time.

5. How Does a Buy to Let Mortgage Work

It is highly likely that you will want to finance the purchase of your buy to let properties. Leveraging the bank’s money is a very good idea.

Buy to let mortgage rates are at an all time low at the moment, it is a great time to take advantage of this.

However, don’t just rely on offers from high street banks, take the time to research all avenues.

Find a Great Buy To Let Mortgage Broker

I strongly recommend you find a great mortgage broker (or more than one if you can) and make them a member of your virtual buy to let investing team.

Mortgage brokers are often a good bet as they’ll offer you a broader range of options, than just high street banks, and will be able to help you weigh up what’s best for your individual needs.

Their job is to find the best buy to let mortgages for you.

One of the top tips for being a successful buy to let investor that I can offer you is to work with experts. Having a great mortgage broker is vital to your success, choose one you can share your property investment goals with.

They can compare all of the buy to let mortgage options and find you the best rate or the best mortgage for your circumstances. Building a relationship with your broker will help you every step of the way.

If you are new to buy to let mortgages then often you will pay more for them compared to a conventional residential mortgage. But don’t let this put you off, as the rental income should cover the mortgage costs.

How Much Deposit on a Buy To Let

In terms of the deposit on buy to let, you can expect to have to find anywhere from 25% to 40% of the purchase price of the investment property.

A lot of property investors tend to go for interest only buy to let mortgages. With this kind of mortgage, you just pay the interest on the loan each month.

You will pay back the capital amount when the mortgage ends. Landlords tend to cover monthly mortgage payments from the rent that they receive from their tenants.

The amount that you can borrow with a buy to let mortgage will depend on the deposit that you make, the estimated rental income and your specific circumstances.

Any lender is going to want to see that the rent that you receive will more than cover your mortgage repayments. You want to see this too.

Compare Buy to Let Mortgages

You can use a service like moneyfacts.co.uk to find and compare buy to let mortgages.

Best Buy To Let Mortgage Rates

Buy to let mortgage rates will vary from lender to lender. As a guide, you can expect a buy to let mortgage to have an APR of between 3% and 4%. Lenders will calculate the rates taking into account the deposit amount and other factors.

You can use an online buy to let uk mortgage calculator which should make it easier for you to accurately estimate what your mortgage repayments will be.

If you are looking online for one of these helpful calculators, then make sure you look for a buy to let mortgage calculator UK.

Usually, a buy to let mortgage will have a full term of 25 years and will generally come in two main types, fixed or variable. Fixed the rate stays the same for the first 1, 2 or 5 years, variable can go up and down depending on the current Bank of England Base Rate.

There are many other buy to let mortgage options, for example; trackers, first time buyer mortgages, 80% LTVs etc. Some lenders have upper age limits for borrowers and others don’t.

This is why it is vital to speak with a good buy to let mortgage broker, the options are endless, and you need to find the best one for your circumstances.

6. Buy to Let using a Limited Company

With so many changes over recent years to the buy to let market, one of the most sensible investment approaches is to use a limited company.

Many landlords have indicated that they want to move to a limited company structure to invest in rental properties in the near future.

You need to understand the ins and outs of this so please read on.

So why should you use a limited company for buy to let investment?

Well, you can create a Special Purpose Vehicle (SPV) through a limited company which you only use for property investment. This is a clean solution favoured by the majority of lenders.

There are a few advantages to using a limited company and SPV and some disadvantages too.

Advantages:

- Lower rate of tax on rental income – if you are in the highest 40% tax bracket compared to 20% corporation tax

- You can treat mortgage interest as an expense to offset corporation tax

- You can use an SPV to broker JV deals cleanly

- Most mortgage lenders will work with clean limited companies set up as SPV’s

Disadvantages:

- Profits are taxed and so are dividends and any director drawings

- The process for arranging mortgages is longer

- Mortgages tend to be more expensive

While you could approach mortgage lenders directly to obtain a mortgage with your limited company, I recommend that you use the services of a competent mortgage broker.

They will have experience of finding the best mortgage offers for limited companies.

-

Using an SPV for buy to let investment is relatively new

Using an SPV for buy to let investment is a relatively new way of working so the process is still fairly slow with 6 to 8 weeks being the average time at present.

This will be a problem if you are under time pressure to make a purchase such as at an auction for example.

The other thing that you need to be aware of is that mortgages tend to be more expensive for limited companies than they do for individuals. Also, the norm is 75% loan to value.

You can go for a higher loan to value but this will certainly incur additional costs.

My advice is to set up your limited company SPV as this will be a lot more attractive to mortgage lenders.

A lender will expect an SPV to be a relatively new entity and have a specific Standard Industrial Classification of Economic Activities (SIC) codes either:

- 68100 buying and selling of own real estate

- 68209 other letting and operating of own or leased real estate

Mortgage lenders will undertake background checks on the applicants and the directors (if different). Lenders are looking at a potential landlord’s ability to overcome challenges such as planned renovations, voids and other buy to let risks.

You don’t want your limited company to have traded before in another industry.

This will complicate matters when it comes to borrowing money so we recommend that you create a brand-new company for buy to let investment only.

Different lenders will insist on different security arrangements to lend money to an SPV. Here are the most likely scenarios:

Personal Guarantees

The lender may require the directors to provide personal guarantees that they will cover any outstanding expenses after selling the property if there is a default on a loan.

Debenture

This will impose floating or fixed charges if there is a loan default or the company becomes insolvent.

Deed of Priority

This is an agreement about who will be first in the queue if there are more than one lender involved with an SPV.

7. Four Critical Things Buy To Let Investors Need to Know

There are often changes in the buy to let sector.

The government and local councils make these changes because they want landlords to be more professional and offer a good standard of accommodation to their tenants.

Landlords need to do all that they can to take care of their tenants. This starts with the standard of accommodation that they provide and extends to safety and having the right documentation in place.

A recent survey by Direct Line showed that some landlords had significant knowledge gaps in 4 areas:

1. The Tenancy Agreement

In the survey by Direct Line, nearly 60% of new landlords said that the most difficult aspect of successfully renting out their buy to let property was the creation of a good tenancy agreement.

The tenancy agreement is very important as it is a binding contract between you as the landlord and the tenant.

While it is possible to have a verbal tenancy agreement this is uncommon and not recommended. A good tenancy agreement needs to be in a written document.

Your tenancy agreement needs to specify the term of the let. This could be a fixed term of 6 months or a year, or a periodic tenancy which runs on month to month or even week to week.

You have a few choices when it comes to creating a tenancy agreement:

- Pay a solicitor to create one for you

- Pay your letting agent to create one for you

- Download a tenancy agreement template and modify it to suit your requirements

- Use documents provided by the NRLA

It is very important that you have a good tenancy agreement in place so choose the method that works best for you.

2. Deposits

Deposits are another area where new landlords admitted a lack of knowledge in the survey – almost 50% of the participants admitted that they needed to improve their knowledge in this area.

There are several things that a tenancy security deposit has an impact on and this includes evictions.

The first thing you need to know is that you have to use an approved scheme for tenancy deposits. Approved TDP schemes include:

Tenants are entitled to get their deposits back if they have honoured the terms of the tenancy agreement. As a landlord you can reasonably make some deductions such as property damage and unpaid rent.

3. Evicting Tenants

More than 50% of the new landlords in the survey said that their knowledge of evictions was weak. With the Covid-19 pandemic this is a hot subject as the government has acted to provide protection to tenants so prevent evictions.

You need to be fully aware of where you stand with evictions and the law.

4. Damage to Property

There were around 23% of new landlords in the survey that admitted their knowledge about property damage was lacking.

The biggest area of concern for these new landlords was the difference between damage that is unreasonable and what constitutes fair wear and tear.

On the Shelter website there is a good article on this. They believe that the day to day use of a rental property can lead to “damage” which landlords should not penalise the tenants for.

This could be paint peeling due to bad weather or a new carpet which has clear signs of use for example.

8. Finding Great Tenants and Managing Your Properties

If you are going to invest in buy to let properties that are outside of your local area then you should consider hiring a good letting agent to take care of finding tenants for you and property management.

A buy to let property without a tenant will not make any money for you

Yes, this is obvious, but you want to avoid “vacant time” with all of your buy to let properties as much as possible.

Good local letting agents will know the best tenant demographics for your property and where to find them quickly. They will know what rental prices you can charge for the accommodation that you are offering.

Make it your business to discuss your property investment plans with letting agents in your preferred locations.

As a landlord, you have a responsibility to ensure that the upkeep of your property is maintained. If a tenant has a problem with the heating and you are 200 miles away then you are not going to be able to respond quickly.

Your tenants will not appreciate this.

There are many other things that a good letting agency can do for you such as the drawing up of tenancy agreements and checking to ensure that your properties are all in compliance with local laws and regulations.

It is an additional cost but it is often the best way to go if you do not live in the area where your buy to let property is located.

1. What is a Buy to Let?

2. Is Buy to Let worth it in 2022?

3. How to Choose the Best Place to Buy to Let

4. It is Vital to Carry Out Buy to Let Deal Analysis

5. How Does a Buy to Let Mortgage Work

6. Buy to Let using a Limited Company

7. Four Critical Things Buy To Let Investors Need to Know

8. Finding Great Tenants and Managing Your Properties

My Final Thoughts on Buy To Let Investing

Buy to let investing in the UK is still worth it in 2022. Follow the golden rules in this buy to let strategy guide and you will have a very good chance of success. You need to look for places in the country that offer the best rental yields and have the best development prospects to ensure that you can achieve the maximum buy to let returns.

I know several people who started this and ended up doing it full-time. A family friend actually became a millionaire in just 10 years of buying up properties and renting them out. She works with commercial and residential housing. I feel like 2021/2022 is going to be a prime time to buy as these inflated house prices will come down and a lot more houses will be available on the market. I am working on getting into this myself. Loved the article, it answered all my questions and more. Can’t wait to buy my first house and rent it out!

Awesome thank you Matt. I’m really glad you found the article useful. Good luck on your real estate investing journey.

Kind Regards

Harvey

Letting, or well “renting’ as we refer to it around here, has been a pretty solid market for a lot of people. I know several people who quit their 9 to 5 and found great opportunity in buying up homes on the low and then fixing them up to rent out. I have considered it but I have always been rather cautious with my investments. You gave some pretty sound information here though. I am really considering buying a house near the end of summer to work on in the fall and winter months.

Thank you Michael for your comment. I’m glad you found the information useful. I would say go for it, I’m sure you will not be disappointed in the long run. Good Luck 🙂